Often the benefits of the R&D tax incentive are misunderstood.

Is it a super tax credit, cash back or extended loss?

Is the R&D benefit 43.5%, 18.5%, I have also heard 16.5% and 8.5%.

In truth, all the above are correct, but in different scenarios.

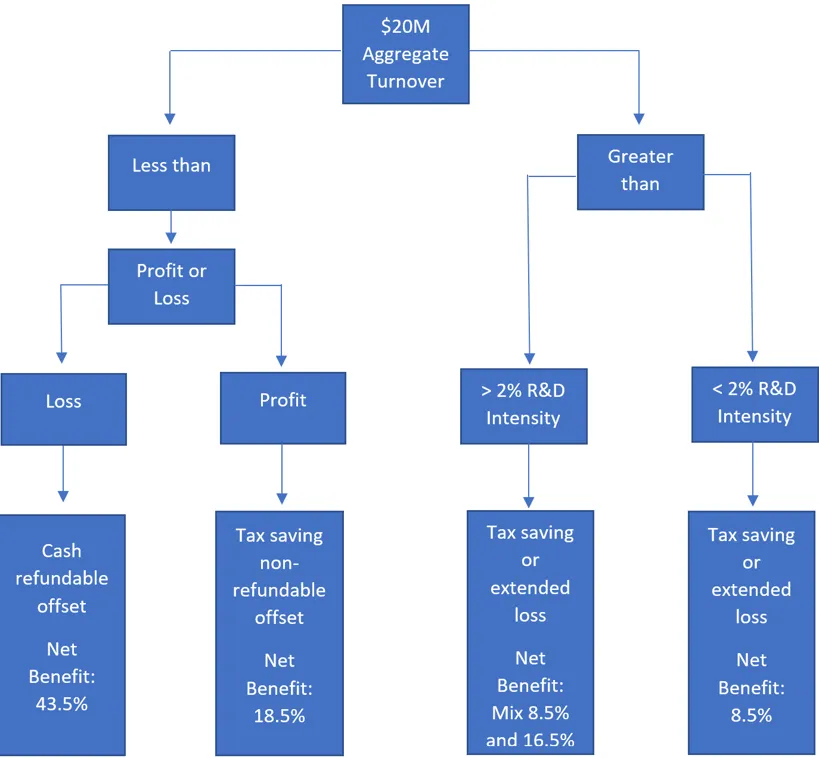

The first point to consider is whether your business is or above the $20 million aggregate turnover threshold.

For R&D entities with an aggregated turnover of less than $20 million, the refundable research and development tax offset is your corporate tax rate plus an 18.5% premium.

For R&D entities with an aggregated turnover of $20 million or more, the non-refundable research and development tax offset is your corporate tax rate plus an incremental premium.

The premium increments are based on your R&D Intensity. This is a percentage of your eligible R&D expenditure as a proportion of your total expenditure for the year.

The table and diagram below explain the different benefits and R&D intensities.

R&D BENEFIT SUMMARY:

R&D BENEFIT DIAGRAM:

Think you might be eligible? We have put together some basic questions for you to quickly find out!

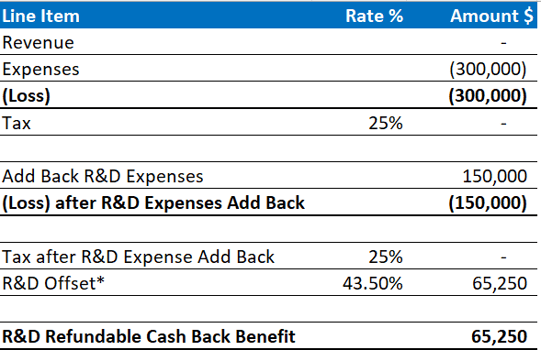

BENEFIT 1: CASH BACK BENEFIT

The refundable cash back benefit is reserved for loss making entities.

Explained briefly, if your company has enough current or accumulated losses (losses from prior operating years) available then the R&D tax incentive allows the company to “dip into” its losses and “cash them in” in the current year as opposed to waiting until future, profit making years, in order to not pay tax.

This benefit is an absolute lifeline to innovative companies who are yet to break even or are in a pre-revenue stage.

Our example below assumes zero revenue however the same principles can be applied to companies with revenue who have current or accumulated losses.

* The research and development tax offset is calculated by taking the R&D eligible expenditure (in this example that figure is $150,000) and multiplying it by the appropriate R&D tax incentive rate of 43.5%. Our example entity would have received $65,250 in cash from utilising the R&D tax incentive.

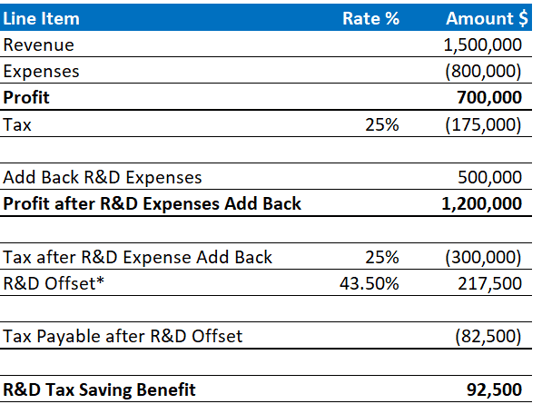

BENEFIT 2: TAX SAVING BENEFIT ENTITY < $20M in AGGREGATE TURNOVER

* In our example, we have a revenue and profit-making entity with an aggregate turnover of less than $20M. The research and development tax offset is calculated as 43.5% of the R&D expenditure of $500,000, giving us an offset of $217,500.

The R&D benefit is calculated as the original tax payable by the company of $175,000, less the tax payable after utilising the R&D tax incentive, being $82,500. This yields a net R&D benefit of $92,500, which will be realised as a tax saving.

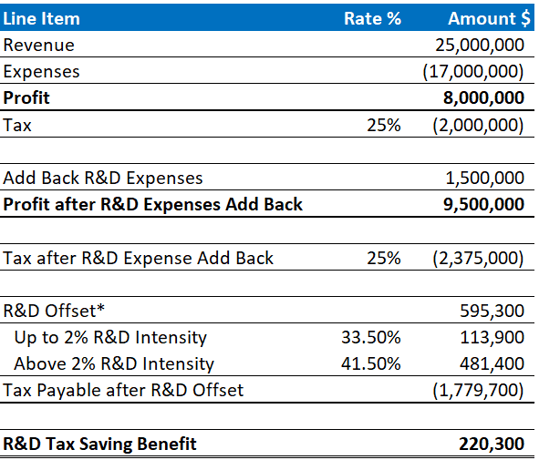

BENEFIT 3: TAX SAVING BENEFIT ENTITY > $20M in AGGREGATE TURNOVER

* In our example we have a revenue and profit-making entity with an aggregate turnover of greater than $20M.

The R&D tax incentive benefit for an entity with > $20M is dependent on the R&D intensity of the company and is a non-refundable offset.

In other words, the R&D benefit for such an entity is restricted to a non-refundable tax saving or extended losses.

The entity in our example has > 2% R&D intensity and therefore their benefit is a hybrid of up-to 2% intensity at a 33.5% benefit and a greater-than 2% intensity at a 41.5% benefit.

The research and development tax offset is calculated as the hybrid rate on the R&D expenditure of $1,500,000, giving us an offset of $595,300.

The R&D benefit is calculated as the original tax payable by the company of $2,000,000, less the tax payable after utilising the R&D tax incentive, which is $1,779,700. This yields a net R&D benefit of $220,300, which will be realised as a tax saving.

An important point to note is that as of the 2022 Financial Year, the benefit for companies with > $20M changes to a new 2-tiered approach.

Our experiences at Rimon Advisory have shown that the R&D tax incentive has been exceptionally beneficial to our clients of all sizes, from early-stage companies to established SMEs, all the way through to listed entities.

Lior Stein is the Co-MD at Rimon Advisory, a leading Australian R&D Tax Incentive and Export Market Development Grant consulting firm.

You may be interested to know if your business could use the R&D Tax Incentive.

We have put together a few quick questions for you to be able to assess your eligibility.

Click below if you want to know more: